Homeowners are having trouble with large repayments and decreased savings as a result of rising interest rates. Also, banks and mortgage companies are raising interest rates as a result of inflationary pressures (Australian Institute of Health and Welfare, 2024). It further reduced the profit margins for homeowners, which is emerging as a financial burden for them.

Trend of housing affordability

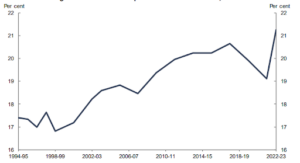

Recent statistics showed that rising interest rates and housing prices have significantly decreased housing affordability, as reflected below:

Figure: Rising housing prices in Australia

(Source: National Housing Supply and Affordability Council, 2024)

As depicted above, the rate of mortgage increase from 2010 to 2022 resulted in a fall in housing affordability for homeowners. With an average increase of 125 points in 2023, it has grown to be a significant concern (National Housing Supply and Affordability Council, 2024). This is where mortgage restructuring and consolidation can help manage high interest rates and savings.

Mortgage Consolidation & Restructuring

Mortgage consolidation is a way in which homeowners can combine multiple debts into one. This will help them improve savings in the era of high interest rates by paying a low interest rate for the consolidated debt. However, mortgage restructuring is the process by which you can renegotiate the terms of the mortgage with the lender. Here is the process that you can go with for consolidation and restructuring:

How to go with it?

- Examine your financial goals: Firstly, you need to understand your financial goals and why you want mortgage consolidation or restructuring. Do you want to lower the interest rate or do you want to gain other features to improve your savings on interest or something else? This will guide you in your search for better refinancing options and provide you with knowledge of your current mortgage.

- Evaluate the current financial situation: Then, you need to evaluate your current financial situation, including pending home loans, credit cards, and personal loans. It will help you choose the right option for you in terms of either going with restructuring or consolidating debts.

- Assessing refinancing options: Afterwards, you need to find a trustworthy mortgage broker for consultation on refinancing options. This will improve your decision-making in choosing the right option for you, considering the costs involved in each option with benefits.

- Application for a new refinancing loan or amendments: After knowing the correct refinancing options, either apply for a new loan or restructure your mortgage. You can also consolidate your debts for an existing loan by providing necessary documents, including loan statements, credit history, and proof of income.

- Implement the strategy: Whatever strategy you have selected for refinancing in terms of consolidation or restructuring, go with it. When it gets approved, work on managing the new loan structure. You can even use automated payments to not miss the repayments.

- Regular review and monitoring: Do periodic reviews of all your finances to ensure they meet your financial requirements. Further, if you select consolidation of debts, make a single payment for your new loan.

This way, you can either consolidate or restructure your finances, which will benefit you in savings while managing high interest rates.

Why go for these options?

Mortgage consolidation and restructuring can offer you tremendous benefits to beat the worries of high interest rates. It will improve your savings in such a way that you can gain maximum financial outcomes during the inflationary market.

This will further help you lower your monthly payments, as you just need to pay for a single mortgage through consolidation of debts while managing your other expenses too. However, if you choose to restructure, then you can negotiate your terms for the loan again and seek more time for repayments, which will help reduce the financial burden.

Consolidation of debts will also assist in improved cash flow, as you can save funds that were previously used to pay high interest rates. It will help you manage savings and open other options for financing for you. This will further save your financial future during economic downturns.

On the other hand, restructuring will help you protect your position to be listed in the list of defaulters. This will further foster the lender’s trust in you, which will benefit you in gaining more options for financing, thereby reducing financial distress. Alongside this, you can seek the benefits of home equity while consolidating debts. It will reduce high-interest-rate loans with maximum savings.

When to go for consolidation or restructuring?

Decisions for refinancing need thoughtful moves, like whether to go for consolidation or restructuring. Here are a few tips you can take as a guide for making this decision:

- Difficulty in managing multiple high-interest debts: When you struggle to manage multiple high-interest debts. Then, in this case, consolidation will be a good choice for you. It will significantly assist in reducing interest rates with easy management of your monthly repayments.

- Manageable home equity: You can also go with consolidation when you have enough home equity to access the required funds. Usually, lenders consider 80% of property value while lending money, so you need to prepare yourself for it.

- Want flexibility: If you want flexibility with your current loans, then you can go for restructuring, where you can switch to a more suitable mortgage option. This will help you match your ability to repay and earn more savings compared to your existing mortgages.

- Opportunity of better terms: If you get the opportunity of better interest rates, you can seek the benefit of this to restructure your portfolio with maximum savings.

How to avail benefits of them?

Consult a trusted financial broker to explore the best consolidation or restructuring options and get expert advice catering to your needs. This will sound your decision-making process, giving you a worry-free future apart.

You can consult experts at Nfinity Financials for a better guide. We will be glad to assist you in every possible way.

For loan and mortgage advice, you can also contact us at 1300 GET LOAN or 1300-438-562 or 0456 456 267.